Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Is the Crypto Industry Really in Trouble with the Market This Bad?

Original Article Title: False Narratives....and Other Thoughts

Original Author: @RaoulGMI

Translation: Peggy, BlockBeats

Editor's Note: As market sentiment continues to weaken, cryptocurrencies are repeatedly labeled as reaching the "end of the cycle." However, this article believes that the price decline is not due to fundamental failure but rather a result of a temporary liquidity squeeze. The reconstruction of the U.S. Treasury's account, exhaustion of reverse repo tools, government shutdown, and the strengthening of gold have collectively diverted funds that should have flowed into high-duration assets, putting pressure on assets such as Bitcoin and SaaS.

At the same time, the "false narrative" surrounding monetary policy is also cause for concern. While the market generally views Kevin Warsh as a hawk, statements from Druckenmiller indicate that his policy approach is closer to the Greenspan era: allowing the economy to run hot and betting on productivity gains to mitigate inflation. Within this framework, future developments are more likely to involve rate cuts and coordinated liquidity release on the fiscal side.

In a full-cycle perspective, time is often more important than price. In the short term, risk assets may continue to be under pressure; but as liquidity constraints are gradually removed, the current pessimistic narrative may be repriced.

The following is the original article:

False Narratives....and Other Thoughts

I wanted to share some insights I gained while writing GMI this weekend, hoping to help stabilize your emotions and regain some confidence. Sit tight, pour a glass of red wine or grab a cup of coffee.... These are the types of insights I would normally reserve for GMI and Pro Macro, but I know you really need to be comforted right now.

"Grand Narrative"

The popular grand narrative right now is: Bitcoin and the entire crypto market have broken down. The cycle has ended, everything is screwed, and we can never have nice things again. It has completely decoupled from other assets—blame it on CZ, blame it on BlackRock, blame it on someone else.

Frankly, this is indeed a highly tempting narrative trap... especially when you wake up every day to see prices plummeting and crashing over and over again.

But yesterday, a GMI hedge fund client sent me a brief message, asking me: Is now the time to buy SaaS stocks? They have dropped very cheaply; or is it, as the current narrative implies, that Claude Code has "killed" SaaS?

So I decided to do some serious research. What I found blew apart the "BTC is dead" narrative and the "SaaS is done" narrative in one fell swoop.

Because the charts of SaaS and BTC are identical.

UBS SaaS Index vs Bitcoin

This means there is another factor at play that all of us have been overlooking...

This factor is: Due to two shutdowns and issues at the systemic "pipeline" level of the U.S. financial system, liquidity in the U.S. has been continually suppressed. (The "water release" of the Reverse Repo tool was actually largely completed in 2024)

As a result, the July and August rebuild of the TGA (U.S. Treasury General Account) did not have a corresponding currency hedging mechanism.

The result was a direct drain of market liquidity.

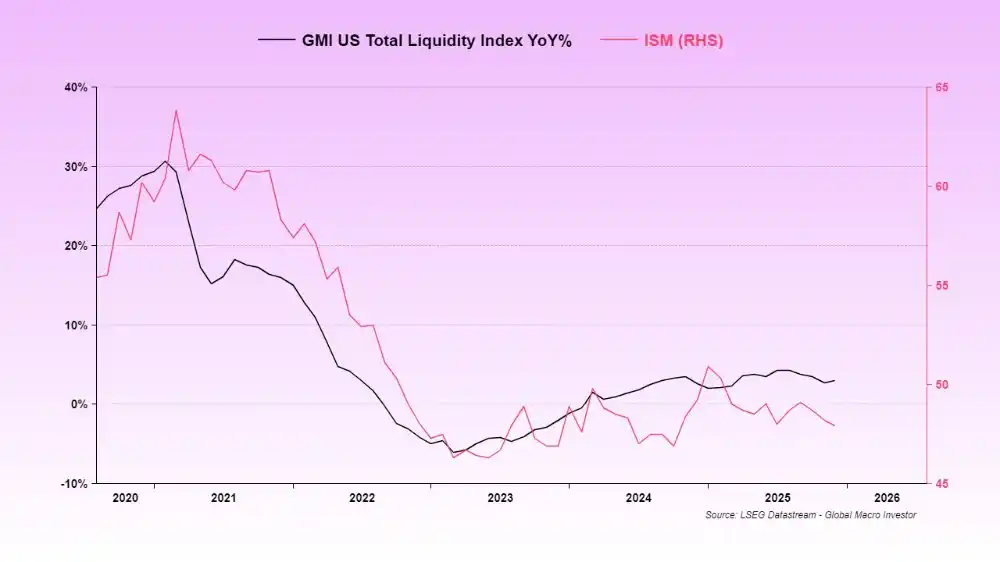

The consistently weak liquidity so far is the reason why the ISM index has remained low.

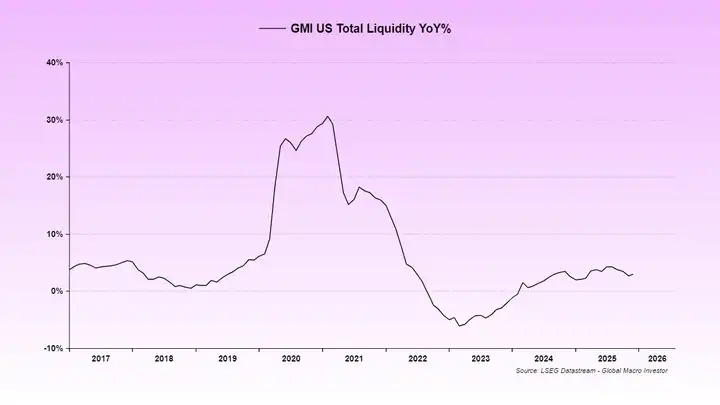

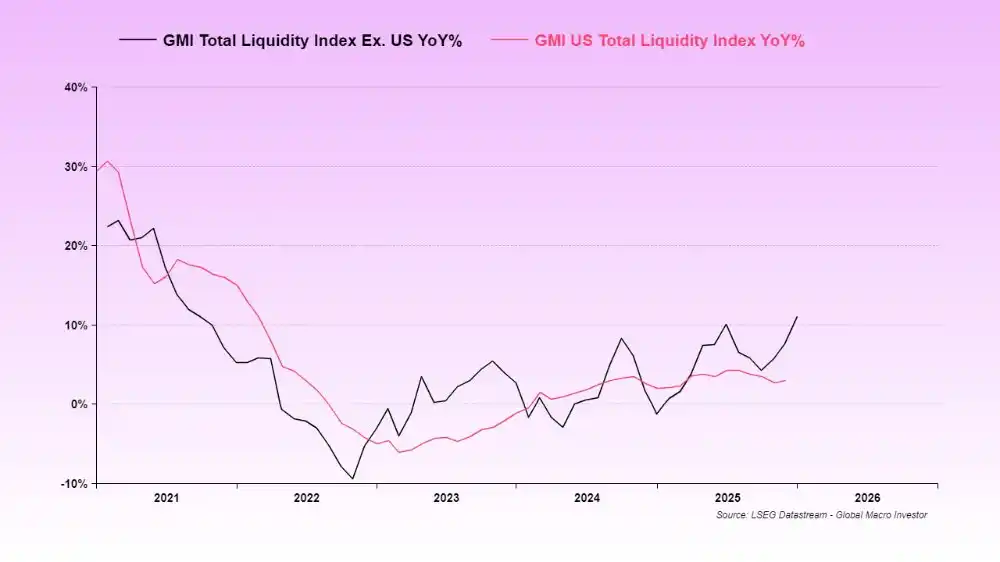

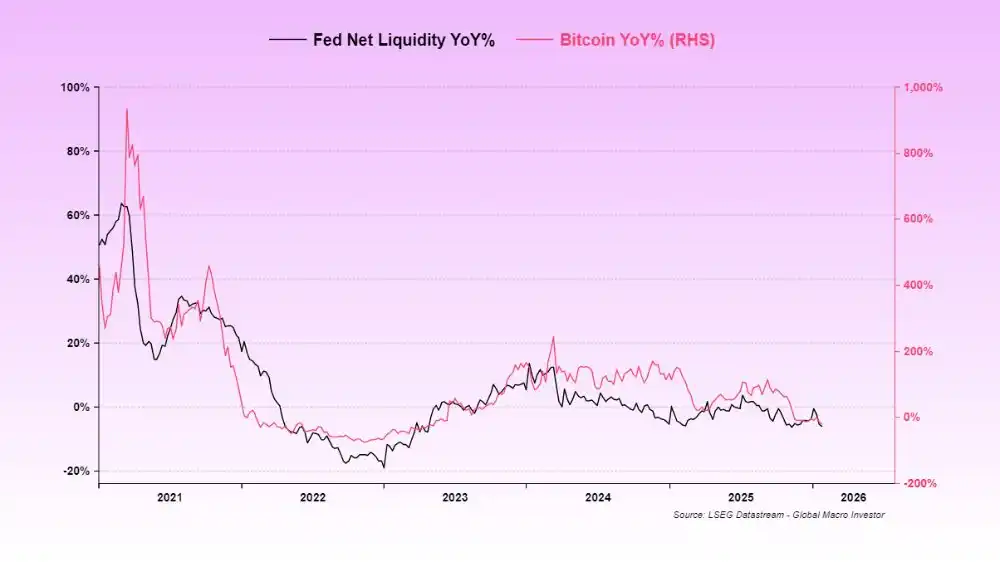

We usually look at the Global Total Liquidity (GTL) because over the long term, it's most correlated with BTC and the Nasdaq Index (NDX).

But at this stage, U.S. Total Liquidity (USTL) is clearly more dominant—because the U.S. remains the core supplier of global liquidity.

In this cycle, the Global Total Liquidity (GTL) has led the U.S. Total Liquidity (USTL) in terms of change, and the upcoming liquidity recovery is approaching—ISM will also warm up accordingly.

And this is the key reason impacting SaaS and BTC.

These two asset classes are essentially the longest-duration assets; when liquidity experiences a temporary retreat, they will naturally be revalued at a discount overall.

Meanwhile, the rise of gold has almost absorbed all marginal liquidity in the system — the funds that were originally supposed to flow into BTC and SaaS were intercepted by gold.

When liquidity is insufficient to support all assets simultaneously, the riskiest part will be the first to take a hit.

This is the reality of the market.

Now, the U.S. government has once again shut down.

The Treasury Department actually hedged against this: after the last shutdown, it did not use the funds in the TGA (Treasury General Account); instead, it continued to put money in — which further drained market liquidity.

This is the "liquidity drought" we are currently facing, which is why the price action is so brutal.

There is currently no liquidity available to flow into our beloved crypto market.

However, signs indicate that this shutdown is likely to be resolved this week, and this will be the last liquidity barrier to cross.

I have mentioned the risk of this shutdown many times before. Soon, it will be a picture in the rear-view mirror, and we can truly enter the next phase — a liquidity flood driven by factors such as eSLR adjustments, partial TGA release, fiscal stimulus, rate cuts, etc.

Ultimately, all of this revolves around the midterm elections.

In a full-cycle trade, many times, "time" is more important than "price." Yes, the price may take a harsh beating; but as time extends and the cycle continues, everything will self-correct, and the "alligator jaws" will eventually close.

This is also why I repeatedly emphasize "PATIENCE."

Things need time to unfold, and staring at your P&L every day will only harm your mental health, not improve your portfolio performance.

About the Fed's "Misnarrative"

Speaking of rate cuts, there is still a widely circulated misnarrative in the market: that Kevin Warsh is a hawk.

This is completely nonsense.

These claims are mainly based on remarks from 18 years ago. Warsh's duty and mission are to replicate the Greenspan era's playbook. Trump has said this, and Bessent has also said so.

The detailed elaboration is too long, but the core meaning is only one: rate cut to make the economy run hotter, while assuming that the productivity boost from AI will suppress core CPI. Just like in the 1995–2000 period.

Warsh indeed dislikes balance sheet expansion, but now the system has hit the reserve constraint, so he is almost impossible to change the current path. If he forcefully changes it, the credit market would be blown apart.

So the conclusion is very simple: Warsh will cut rates, but will not do anything else.

He will make way for Trump and Bessent to use the banking system to drive liquidity. Miran is very likely to forcefully push for a comprehensive reduction of eSLR, giving another push to the whole process.

If you don't believe me, then believe Druck.

Warsh holds a very open and appreciative attitude towards former Fed Chair Alan Greenspan's monetary policy thinking and firmly believes that economic growth can be achieved without triggering inflation

I know that in times when everything seems so bleak, listening to any bullish narrative can feel jarringly out of place. Our Sui position now looks like a pile of dog shit, and we are starting to lose sight of what to believe and who to believe in.

But first things first: this situation, we have experienced many times before.

When BTC drops 30%, it is not uncommon for altcoins to drop 70%; and if they are high-quality assets, the rebound speed is often faster.

Mea Culpa

Our mistake at GMI was: not promptly realizing that "U.S. liquidity" is the true dominant variable in the current stage.

In the past full cycle, it was usually global liquidity that dominated, but this time is different. Now everything is clear — "The Everything Code" is still in effect. There is no such thing as "decoupling".

We just did not anticipate, or underestimated, the cumulative effect of such a series of events: Reverse Repo being drained → TGA rebuild → government shutdown → gold surge → shutdown again.

This combination punch was almost impossible to fully predict in advance, and we indeed underestimated its impact.

But it's all coming to an end now. Finally. Soon, we can return to "business as usual."

We couldn't get every variable right, but our understanding of the situation is now much clearer,

and we remain extremely bullish on 2026 — because we are very aware of the Trump/Bessent/Warsh playbook.

They have told us repeatedly. All we need to do is listen, then be patient.

In full-cycle investing, what truly matters is time, not price.

If you are not a full-cycle investor or cannot handle this level of volatility, that's totally fine.

Everyone has their own style.

But Julien and I have never been day traders, and frankly, we are pretty bad at it too (we don't care about the ups and downs within a cycle).

However, in terms of full-cycle investing, our verified, traceable long-term track record over the past 21 years puts us in the top tier historically.

Of course, a disclaimer: we make mistakes too. 2009 was an excruciating example.

So now is not the time to give up.

Good luck to you, and let's welcome a damn epic 2026 together.

The cavalry of liquidity is on its way.

You may also like

Beta, meet cash flow

How do tokenized stocks work? A conversation with the head of digital assets at BlackRock

Is the rebound an illusion? The bond market has already provided the answer

The End of Crypto Premium? Observing the Market Logic Shift from the Dilemma After Gemini's Listing

The third round of repurchase and destruction by JST has been completed as scheduled, with a repurchase and destruction scale exceeding 21 million USD

Will Bitcoin ETF Increase Bitcoin Price in 2026?

Will Bitcoin ETF increase BTC price in 2026? See what ETF inflows signal about institutional demand, market momentum, and Bitcoin’s long-term outlook.

How to Track Bitcoin ETF Flows in 2026: Best Free Trackers Used by Analysts

Since 2024, Bitcoin ETFs have become one of the main channels through which institutional capital enters the crypto market. Unlike traditional crypto exchange volume data, ETF flow data reflects portfolio allocation decisions from large investors, which often influence long-term price direction rather than short-term speculation.

How to Invest in Bitcoin ETF in 2026: Beginner's Step-by-Step Guide

For users who want the simplest way to follow Bitcoin price movements, ETFs can be a convenient starting point.

What Is a Bitcoin ETF? Is Bitcoin ETF a Good Investment Entry for Crypto Beginners in 2026?

What is a Bitcoin ETF and why does it matter in 2026? Learn how Bitcoin ETFs work, why institutions use them, and how they changed crypto market access worldwide.

Bitcoin ETF vs Ethereum ETF: What's the Difference in 2026?

Bitcoin ETF vs Ethereum ETF: What’s the difference and which should you choose in 2026? Compare risk, adoption trends, and portfolio roles before investing.

The Bounce is a Illusion? The Bond Market Has Answered

The Flip Side of the Stock Market Rally: Energy Reconfiguration, Bitcoin Short Squeeze, and Market Dislocation

Claude's Request for Identity Verification Prompts Reflection from a Relay Operator

PinPet × VELA: Solana's First Atomic Swap Engine and Yield Hedging Protocol, Reframing the DeFi Financial Paradigm

From Coinbase to OpenAI: When lobbying experts start to flee crypto

Understanding the Key Issues of Tokenization in One Article

Silicon Valley Entrepreneurship Guru Steve Blank: In the AI Era, Startups Over Two Years Old Should Reboot

How Dangerous Is Mythos? Why Anthropic Has Decided Not to Release the New Model

Beta, meet cash flow

How do tokenized stocks work? A conversation with the head of digital assets at BlackRock

Is the rebound an illusion? The bond market has already provided the answer

The End of Crypto Premium? Observing the Market Logic Shift from the Dilemma After Gemini's Listing

The third round of repurchase and destruction by JST has been completed as scheduled, with a repurchase and destruction scale exceeding 21 million USD

Will Bitcoin ETF Increase Bitcoin Price in 2026?

Will Bitcoin ETF increase BTC price in 2026? See what ETF inflows signal about institutional demand, market momentum, and Bitcoin’s long-term outlook.