Why Oil Prices Are Rising Again: The Iran Hormuz Crisis and What It Means for Your Portfolio

Prefer us on Google

Prefer us on Google

Oil prices are rising again because the world's most important oil shipping lane is once again in dispute. The Strait of Hormuz, a narrow waterway between Iran and Oman through which roughly a quarter of the world's seaborne oil trade previously passed, has been at the center of an ongoing military conflict since February 28, 2026, when US and Israeli forces launched strikes against Iran and Iranian forces responded by declaring the strait closed and attacking vessels attempting to transit it.

Today's fresh escalation, with US forces striking approximately 90 Iranian targets including air defense systems, coastal radar sites, and missile and drone capabilities, while Iran simultaneously declared the strait closed until further notice and the US military insisted it remained open, has pushed Brent crude above $78 per barrel and sent ripples through bond markets, currency markets, and equity markets simultaneously.

Understanding why the Strait of Hormuz has this kind of power over global financial markets, and what the current escalation means for different parts of a portfolio, is more useful than tracking the day-to-day price movements that the conflict generates.

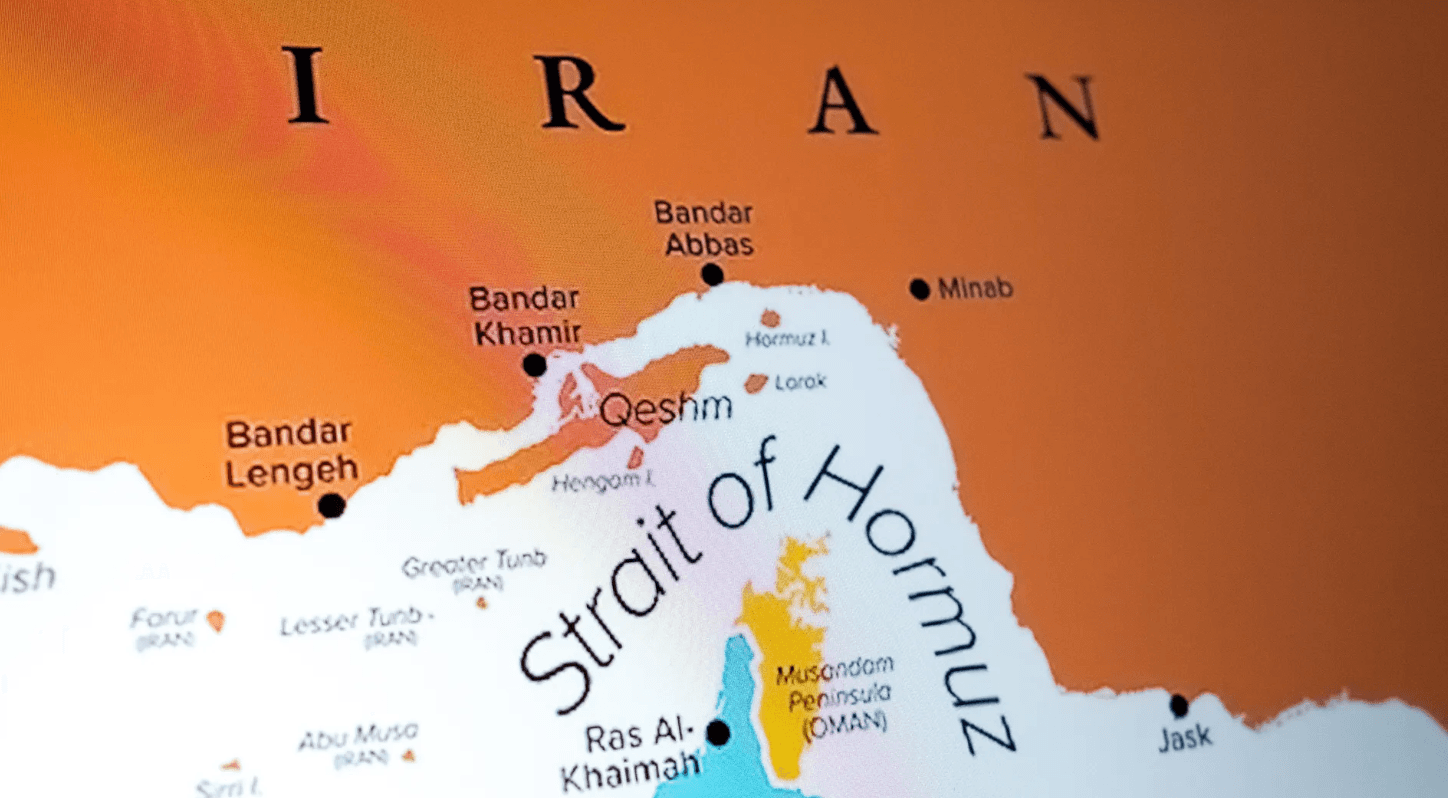

What the Strait of Hormuz Actually Is and Why It Matters

The Strait of Hormuz is a narrow waterway approximately 33 kilometers wide at its narrowest point, separating Iran to the north from Oman to the south, connecting the Persian Gulf to the Gulf of Oman and from there to the Indian Ocean and global markets.

Before the current conflict began in February 2026, approximately 25% of the world's seaborne oil trade and 20% of the world's liquefied natural gas transited this single chokepoint daily. That concentration of global energy trade through a channel that Iran's military can threaten from its northern coastline is the specific geographic reality that gives the Strait of Hormuz its extraordinary financial significance.

There is no practical alternative route for most Persian Gulf oil producers. Saudi Arabia has pipelines to the Red Sea that allow some of its production to bypass the strait. Oman's geography means its exports can reach the open ocean without transiting the most dangerous sections. But Iraq, Kuwait, Qatar, and the United Arab Emirates are largely dependent on the strait for their export capacity. Iran itself controls access to its longest Persian Gulf coastline and has used that geographic advantage as strategic leverage throughout the conflict.

When the strait functions normally, oil markets price in the steady supply flow that approximately 17 to 20 million barrels per day of capacity represents. When the strait is threatened or partially closed, oil markets price in both the immediate supply reduction and the risk premium that uncertainty about future supply creates. That risk premium is what produced oil prices reaching $120 per barrel at the peak of the conflict earlier in 2026, and it is what produced today's more than 3% jump even though US forces are asserting that the strait remains open.

What Has Happened Since February 2026

The current escalation is not a new crisis. It is the latest chapter in a conflict that has been reshaping global energy markets since late February.

When US and Israeli forces launched strikes against Iran on February 28, Iranian forces responded by declaring the strait closed, attacking merchant vessels attempting to transit, and laying sea mines in the waterway. At the height of the disruption, approximately 20,000 mariners and 2,000 ships were stranded in the Persian Gulf unable to exit through the blocked strait.

The economic impact was immediate and severe. Oil prices surged from below $70 per barrel before the conflict to $120 at the peak. Countries most dependent on Persian Gulf oil imports, including South Korea, Japan, China, and India, faced the most acute supply pressure. The United States, as a major domestic oil producer and LNG exporter, actually benefited economically from the crisis through increased export revenues estimated at approximately $50 billion. Russia also benefited through steady export volumes at elevated prices.

A temporary ceasefire reduced tensions and brought oil prices down from their peak. The specific dispute over the strait's status, with Iran insisting on maintaining control over vessel transit and the US demanding a return to pre-war maritime norms, was never fully resolved. Today's escalation reflects the underlying negotiating gap that was always present beneath the surface of the temporary calm.

The specific trigger for today's fresh exchange of strikes is the status of that negotiating gap. Iran has maintained that giving up control over strait transit would amount to surrender. The US has insisted that freedom of navigation through the international waterway is non-negotiable. With Qatar and Pakistan attempting to mediate and bring the parties back to negotiations, today's military exchange represents the collapse of the diplomatic momentum rather than the opening of a new phase of conflict.

What Rising Oil Prices Do to Different Parts of a Portfolio

The financial transmission mechanism from Strait of Hormuz tension to portfolio impact runs through multiple channels simultaneously, and the direction of the impact is different depending on what an investor holds.

Energy stocks are the most direct beneficiary of rising oil prices. Companies that produce oil and natural gas see their revenues increase when commodity prices rise, because their production costs are relatively fixed while their selling price moves with the market. The major integrated oil companies, independent producers, and oilfield services companies all benefit from sustained higher oil prices. In the current environment, US-based energy companies benefit additionally from the substitution demand created when Persian Gulf supply is disrupted and buyers look to US LNG and crude exports as alternatives.

Transportation and consumer discretionary stocks are the most direct victims. Airlines pay for fuel directly in jet fuel that prices off crude oil. Shipping companies face higher bunker fuel costs. Consumer spending on gasoline reduces discretionary income available for other purchases, which pressures retail, restaurants, and entertainment spending. Automotive companies face both higher production costs and lower consumer willingness to buy vehicles when gasoline prices are high.

Technology stocks have an indirect relationship with oil prices that runs through inflation and interest rates. Higher oil prices feed into headline inflation, which complicates central bank decisions about when to cut interest rates, which affects the discount rate applied to technology companies' future earnings. Technology companies trading at elevated multiples are particularly sensitive to interest rate expectations because a higher discount rate reduces the present value of earnings that arrive years in the future. Today's US Treasury yield increase, with the two-year bond rising to its highest level since February 2025, reflects exactly this transmission mechanism.

Asian markets and Asian market-exposed stocks face specific and acute pressure. South Korea's KOSPI circuit breaker today was partly a function of the oil price shock's direct economic impact on a country that imports more than 80% of its crude. Japanese equities face similar pressure. Companies with significant revenue exposure to Asian markets, particularly in manufacturing and consumer goods, face the compounded pressure of Asian market weakness and margin compression from higher energy input costs.

Gold, Bonds, and the Dollar: Where Money Flows When Hormuz Is in Crisis

The Strait of Hormuz crisis also affects the safe-haven asset dynamics that determine where capital flows when equity markets experience stress.

The US dollar has strengthened against all G10 currencies today. That dollar strengthening reflects the classic flight to safety that geopolitical risk events produce. The dollar is the world's reserve currency and the currency in which oil is priced globally. When oil supply is disrupted and geopolitical uncertainty rises, demand for dollars increases both for oil purchasing and for safe-haven holding purposes.

Gold typically rises in geopolitical risk environments as investors seek assets that are independent of any single government's creditworthiness or the functioning of international financial systems. Oil supply disruptions that threaten global economic stability are specifically the kind of scenario that gold's historical safe-haven role was established to address.

Government bonds present a more complicated picture in this specific crisis than in a typical risk-off event. US Treasury yields rose today rather than falling, which is the opposite of the typical safe-haven bond response to equity market stress. The reason is inflation. Oil price spikes create genuine inflation pressure that makes central banks less likely to cut rates even when economic uncertainty is rising. Higher inflation expectations produce higher bond yields, which means the Treasuries that would normally benefit from a flight to safety are simultaneously being sold by investors pricing in a more persistently inflationary environment.

This unusual combination, rising oil, rising gold, rising dollar, and rising bond yields simultaneously, is the specific financial market signature of a geopolitical oil supply crisis rather than a pure financial stress event. Investors who understand that signature can position portfolios more accurately than those who apply the standard risk-off playbook that works for recessions and financial crises but not for energy supply disruptions.

The Specific Stocks and Sectors Affected Today

Beyond the general transmission mechanisms, today's escalation has specific impacts on identifiable stocks and sectors that are worth naming rather than discussing in the abstract.

The semiconductor sector, which drives both the KOSPI and a significant portion of the Nasdaq, faces pressure from two directions. Korean semiconductor manufacturers including SK Hynix and Samsung face both the direct cost pressure from Korean won weakness and the indirect pressure from reduced corporate earnings estimates as Korean energy costs rise. US semiconductor companies face the interest rate transmission mechanism, where higher oil-driven inflation complicates the rate cut expectations that have supported elevated technology valuations.

Airline stocks are the most directly impacted US equity names. Jet fuel represents 20% to 30% of airline operating costs, and a sustained 3% to 5% increase in oil prices reduces airline earnings estimates by amounts that show up immediately in stock prices. Airlines that have hedged their fuel costs have partial protection, but hedges have finite duration and only delay rather than eliminate the impact of sustained higher prices.

Refiners present the counterintuitive case where rising crude prices can actually benefit margins, depending on the crack spread between crude input costs and refined product prices. When crude rises faster than refined products, refiners are hurt. When refined products rise faster than crude, as can happen when supply disruptions create regional product shortages, refiners benefit. The specific geometry of the current disruption, with the Strait of Hormuz affecting crude flows more than refined product flows initially, creates a specific crack spread dynamic that experienced energy investors will be tracking.

What Citibank and the Oil Market Are Saying About Resolution

The current consensus among energy market analysts is that full strait closure is not what oil markets are pricing in, despite the conflicting statements from Iran and the US about the waterway's status.

Andy Lipow of Lipow Oil Associates described the oil market as pricing in a new normal where periods of conflict occur between periods of relative calm that permit tanker transit. That framing captures something important about how the market has adapted to the ongoing crisis. Rather than pricing in a binary open or closed strait, the market is pricing a probability distribution of outcomes where some transit occurs, some disruption occurs, and the balance between them fluctuates with military and diplomatic developments.

Citibank analysts told clients that the US and Iran are likely to return to negotiations within weeks, because both sides have too much to lose from a spiral of escalation that destroys regional energy infrastructure. The specific argument is that Trump's preference for strong equity prices and stable bond markets creates a financial market pressure on the administration to seek de-escalation. When oil prices rise and equities fall on Middle East news, the administration faces market feedback that reinforces the case for returning to diplomacy.

Qatar and Pakistan's active mediation efforts provide the diplomatic channel through which a return to ceasefire is most likely. The specific conditions for that return, with Iran insisting on maintaining some control over strait transit and the US insisting on pre-war maritime norms, represent the negotiating gap that mediation needs to bridge.

For investors, the question is not whether the strait will eventually reopen fully but how long the current elevated uncertainty premium persists in oil prices and what level that premium settles at in the new normal that Lipow described.

For those looking to participate in global financial markets, having access to the right trading platform matters. WEEX offers crypto and stock trading products, covering major global markets including US stocks and digital assets.

Conclusion

Oil prices are rising again because the fundamental dispute over the Strait of Hormuz has never been resolved, only temporarily quieted by a ceasefire that today's military exchange has further strained. The 3% jump in Brent crude to near $79 is not primarily about today's specific strikes. It is about the risk premium that markets attach to supply uncertainty when the world's most important oil shipping lane is controlled by parties in active military conflict.

For portfolio management, the Hormuz crisis creates a specific and unusual financial market environment where energy stocks benefit, technology stocks face multiple headwinds, Asian market exposure carries acute risk, and the standard safe-haven playbook of buying bonds alongside gold does not apply because oil-driven inflation complicates the interest rate picture that normally makes bonds attractive in risk-off environments.

The resolution timeline depends on diplomatic progress that Qatar and Pakistan are currently pursuing. Until a ceasefire framework that addresses the underlying Hormuz control dispute is established, oil price volatility will continue to be a recurring portfolio consideration rather than a one-day event.

FAQ

1. Why are oil prices rising today?

The US and Iran exchanged fresh military strikes overnight, with US Central Command hitting approximately 90 Iranian targets while Iran declared the Strait of Hormuz closed until further notice. The conflicting claims about whether the strait is open created supply uncertainty that pushed Brent crude above $78 per barrel.

2. What is the Strait of Hormuz and why does it affect oil prices?

The Strait of Hormuz is a narrow waterway between Iran and Oman through which approximately 25% of the world's seaborne oil trade previously passed. Iran's military can threaten vessel transit from its northern coastline, giving it strategic leverage over global energy supply that no alternative route can fully replace for most Persian Gulf producers.

3. Which stocks benefit from rising oil prices?

Energy producers, integrated oil companies, oilfield services companies, and US LNG exporters benefit directly from higher oil prices. Gold mining companies and energy infrastructure businesses also benefit. US producers benefit additionally from substitution demand when Persian Gulf supply is disrupted.

4. Which stocks are hurt most by the Iran oil price surge?

Airlines face the most direct impact through higher jet fuel costs. Transportation companies, consumer discretionary stocks, and Asian market-exposed equities face significant pressure. Technology companies face indirect pressure through the inflation and interest rate channel that higher oil prices create.

5. Will oil prices keep rising?

The oil market is pricing a risk premium for strait uncertainty rather than a full closure scenario. Citibank analysts expect the US and Iran to return to negotiations within weeks given the economic pressure on both sides from sustained escalation. Qatar and Pakistan are actively mediating. The specific resolution timeline is uncertain, but the market consensus is that the current elevated prices reflect uncertainty premium rather than a prediction of permanent closure.

Disclaimer

For informational purposes only. Not financial advice. Any activities, rewards, campaigns, or promotions mentioned do not constitute an offer, solicitation, or recommendation to buy, sell, or trade crypto assets. Crypto assets are highly volatile and may lose value. WEEX services, products, or campaigns may not be available in all regions. Users are responsible for complying with applicable local laws before participating.

Disclaimer: This content is provided for general branding and informational purposes only and doesn't constitute financial, investment, legal, or tax advice. Any events, rewards, online events, or related information mentioned herein should not be considered a recommendation, solicitation, or invitation to purchase, sell, trade, or otherwise deal in any crypto assets or to use any services. Crypto assets are highly volatile and may result in loss. WEEX services and online events may not be available in all regions and are subject to applicable laws, regulations, and eligibility requirements. You are responsible for ensuring that your use of WEEX services complies with local laws and for carefully assessing the risks before participating in any crypto-related activities.

You may also like

Introducing Cash Cat ($CASHCAT): Robinhood Chain Meme Token and Price Prediction

Cash Cat is a Robinhood Chain meme token drawing attention after a fast market debut, a 1B supply, and sharp price swings.

LLY Stock Forecast: Can AI and Weight Loss Drugs Drive More Growth?

This article maps how Eli Lilly’s GLP-1 weight-loss franchise and AI-driven R&D could influence LLY’s traditional equity and…

CASHCAT Airdrop: How to Earn Up to 50,000 USDT in Rewards on WEEX

This guide breaks down how the CASHCAT Airdrop works on WEEX, the rewards on the table, and a…

What Is SOXS ETF? The 3X Bear Semiconductor ETF Explained

This guide breaks down SOXS—the Direxion Daily Semiconductor Bear 3X Shares—so you understand what a 3x inverse semiconductor…

Trust Wallet Transaction Stuck or Failed? Here's How to Fix It

A stuck or failed transaction in Trust Wallet is one of the most common problems crypto users encounter and one of the most misunderstood. The cause is almost always related to gas fees or network congestion rather than anything wrong with your wallet. This guide explains why transactions get stuck or fail, how to fix each situation, and how to prevent it from happening again.

Trust Wallet vs MetaMask: Which One Is Better for Beginners?

Trust Wallet and MetaMask are the two most widely used self-custody crypto wallets in the world. They serve different primary purposes and suit different types of crypto users. This guide compares them directly on the dimensions that matter most for beginners making their first wallet choice.

Trust Wallet Seed Phrase: How to Store It Safely and What Never to Do

Your Trust Wallet seed phrase is the single most important piece of information associated with your crypto holdings. Every security measure in the world is irrelevant if your seed phrase is compromised. This guide focuses entirely on storage methods, the specific mistakes that lead to loss, and the habits that protect your seed phrase over the long term.

O Airdrop for New Users: Earn USDT Rewards on WEEX

New to trading O and looking for USDT rewards? This guide explains how the WEEX O Airdrop for…

How to Install Trust Wallet Safely: What Most Guides Leave Out

Most Trust Wallet installation guides tell you where to download the app and how to save your recovery phrase. Few explain the specific mistakes that result in lost funds, compromised wallets, and successful phishing attacks during the setup process. This guide focuses on what those other guides skip.

Samsung Stock vs SK Hynix Stock: Which Korean Memory Giant Is the Better Buy Right Now?

Samsung stock and SK Hynix stock are the two largest memory companies in the world and the two dominant forces in the AI memory boom of 2026. This guide compares the two specifically on the variables that matter for the buy decision rather than on company history or general descriptions.

What Is Trust Wallet? A Complete Beginner's Guide

Trust Wallet is a self custody crypto wallet used by more than 200 million people across more than 100 blockchains. This guide explains what Trust Wallet actually is, how it works, what is new in 2026, and what beginners need to know before using it.

Is Samsung Stock a Buy After Falling 15% From Its All Time High?

Samsung stock is trading approximately 15% below its all time high despite reporting the highest quarterly operating profit ever recorded by a technology company. This guide focuses on the buy decision specifically, examining what the 15% discount actually represents and whether the business case justifies buying at current levels.

How to Buy Samsung Stock: What Non-Korean Investors Need to Know

Samsung Electronics has no US-listed ADR and no direct equivalent to SKHY on any major Western exchange. Non-Korean investors who want Samsung exposure have four main options, each with different cost structures, accessibility levels, and risk profiles. This guide explains each option precisely and what the tradeoffs actually are.

Samsung Stock Falls 7% on Record Profit: Why 1800% Earnings Growth Was Not Enough

Samsung stock fell roughly 7% on July 7 after reporting Q2 operating profit of approximately $58 billion, a 19 fold increase from the same quarter a year earlier. The result beat analyst estimates. The stock fell anyway. This guide explains the specific mechanism that produced that outcome and what it means for investors watching the July 30 full earnings report.

Iran Crisis and Stock Markets: Which Sectors Win and Which Lose?

The Iran Hormuz crisis has been reshaping sector performance since February 2026. Not all stocks react the same way when oil prices spike. Some sectors benefit directly and immediately. This guide maps which sectors win, which lose, and why the current crisis is producing unusual patterns in some categories.

Bitcoin and the Iran Crisis: Does Crypto Act as a Safe Haven When Oil Spikes?

Oil prices surged more than 3% on July 13 after fresh US-Iran strikes raised new questions about Strait of Hormuz access. Bitcoin and crypto markets responded with characteristic ambiguity. This guide examines whether crypto genuinely acts as a safe haven during oil price shocks, what the historical evidence says, and what the Iran crisis specifically reveals about crypto's role in a geopolitical stress environment.

KOSPI Crash and SKHY: Why South Korean Stocks Fall While US-Listed ADRs Hold

The KOSPI fell more than 8% and triggered a circuit breaker on July 13 while SKHY held near $168 on Nasdaq. The same company's shares moving in opposite directions on two exchanges on the same day is not a contradiction. It is the result of three distinct mechanisms operating simultaneously. This guide explains each one.

What Is a KOSPI Circuit Breaker and Why Has It Triggered Seven Times in 2026?

The KOSPI circuit breaker triggered for the seventh time in 2026 on July 13, halting all South Korean stock trading for 20 minutes after the index fell more than 8%. This guide explains what the circuit breaker is, why it keeps triggering, and what it reveals about the specific structure of the Korean market.

SK Hynix Stock Price Prediction 2026–2030: Can SKHY Reach $500?

SK Hynix stock price is trading at approximately $168 after its Nasdaq debut. Getting to $500 by 2030 requires roughly 198% appreciation over four years. This guide examines what the path to $500 actually requires across four years and three independent growth drivers that operate on different timelines.

SK Hynix Stock Price History: From $40 to $168 in One Year, What Drove the Rally?

SK Hynix stock price was trading near $40 per Korean share equivalent less than a year ago. Today SKHY trades at $168 on Nasdaq after the largest foreign ADR listing in history. This guide maps what drove each phase and what it means for where SK Hynix stock price goes next.

Should You Still Buy SKHY? What SK Hynix Stock's 13% IPO Gain Tells Investors

SK Hynix stock price opened at $170 on July 10 and closed at $168.01, representing a 13% gain from the $149 IPO price. The stock is now trading under its permanent SKHY ticker after switching from SKHYV. This guide focuses on whether the 13% first day gain changes the buy decision and what the current SK Hynix stock price implies about the investment case.

SK Hynix Stock Falls 13% in Korea as SKHY Surges in the US: What Just Happened?

SK Hynix stock fell more than 13% on the Korea Exchange on Monday, triggering a circuit breaker that briefly suspended trading of the entire KOSPI index. This guide explains why the same company's shares moved in opposite directions on two exchanges simultaneously and what it means for investors holding either.

SK Hynix Stock in Korea: Price, Drivers, and How to Buy It

SK Hynix stock (KRX: 000660) is Korea's most valuable listed company on the AI memory boom. See the price, drivers, risks, and how foreign investors can buy it.

Stock Futures Explained: What They Are and How to Trade Them

Stock futures let traders lock in an index price today and preview the market open. Learn how stock futures work, how to read them, and their risks.

BATRA Stock: Price, Forecast, and How to Trade Atlanta Braves Holdings in 2026

BATRA stock explained — Atlanta Braves Holdings price, share classes, 2026 forecast, and how to trade equity exposure via tokenized stocks.

TSMC Stock (TSM): Price, 2026 Forecast, and How to Get Exposure

TSMC stock trades near $434 in July 2026. See TSM's valuation, dividend, analyst price targets, how to buy it, and the key risks before you invest.

GDWR Coin (Global Digital Water Reserve): Legit or Hype?

Is GDWR coin legit? Global Digital Water Reserve is a Solana narrative token with no water backing. See its price, supply, risks, and how to buy safely.

USOH Crypto Scam or Legit? A Complete Risk Analysis

Is USOH Crypto legit or a scam? Explore United States Oil Holdings, its tokenized oil reserve claims, on-chain data, key risks, and investment considerations.

GDWR Crypto Scam or Legit? A Complete Risk Analysis

Is GDWR Crypto legit or a scam? Learn what Global Digital Water Reserve is, review its on-chain data, risk factors, and whether the project is backed by real-world water assets.

AI Stock Outlook: Will Iran Tensions Change the Market Outlook?

Explore how Iran tensions, rising oil prices, interest rates, and Big Tech AI spending could shape the next phase of the AI stock rally.

Introducing Cash Cat ($CASHCAT): Robinhood Chain Meme Token and Price Prediction

Cash Cat is a Robinhood Chain meme token drawing attention after a fast market debut, a 1B supply, and sharp price swings.

LLY Stock Forecast: Can AI and Weight Loss Drugs Drive More Growth?

This article maps how Eli Lilly’s GLP-1 weight-loss franchise and AI-driven R&D could influence LLY’s traditional equity and…

CASHCAT Airdrop: How to Earn Up to 50,000 USDT in Rewards on WEEX

This guide breaks down how the CASHCAT Airdrop works on WEEX, the rewards on the table, and a…

What Is SOXS ETF? The 3X Bear Semiconductor ETF Explained

This guide breaks down SOXS—the Direxion Daily Semiconductor Bear 3X Shares—so you understand what a 3x inverse semiconductor…

Trust Wallet Transaction Stuck or Failed? Here's How to Fix It

A stuck or failed transaction in Trust Wallet is one of the most common problems crypto users encounter and one of the most misunderstood. The cause is almost always related to gas fees or network congestion rather than anything wrong with your wallet. This guide explains why transactions get stuck or fail, how to fix each situation, and how to prevent it from happening again.

Trust Wallet vs MetaMask: Which One Is Better for Beginners?

Trust Wallet and MetaMask are the two most widely used self-custody crypto wallets in the world. They serve different primary purposes and suit different types of crypto users. This guide compares them directly on the dimensions that matter most for beginners making their first wallet choice.